The Regulatory Fog is Finally Lifting

If you're building in fintech or Web3, you know the frustration. One day you're compliant, the next day new guidance appears that sends your legal team scrambling. The regulatory uncertainty around digital assets and cross-border payments has been like trying to build a house while the building codes keep changing.

But here's the thing – the Senate vote on the GENIUS Bill represents a potential turning point. For the first time in years, we might actually get the regulatory clarity that fintech startups, B2B payment platforms, and Web3 companies have been desperately seeking.

What the GENIUS Bill Actually Does

The GENIUS Act (Guidance for Enhanced Administrative Networks and Infrastructures for Unified Stablecoin regulation) isn't just another piece of crypto legislation. It's designed to create a comprehensive framework for stablecoin regulation while establishing clearer guidelines for blockchain regulation in the US.

Think of it as the industry's attempt to move from the Wild West to a well-governed territory – still plenty of room for innovation, but with rules everyone can understand and follow.

The bill addresses three critical areas:

- Stablecoin oversight: Clear requirements for reserves, auditing, and operational standards

- Cross-border compliance: Streamlined processes for international digital asset transfers

- Innovation safeguards: Protections for legitimate blockchain development and deployment

How Web3 Companies Should Prepare

For blockchain and DeFi companies, this isn't just about compliance – it's about legitimacy. The crypto regulation in US has historically been a patchwork of enforcement actions and guidance letters. The GENIUS Bill could change that entirely.

What this means for your Web3 business:

- Clearer development guidelines: No more guessing whether your smart contract design will trigger securities regulations

- Institutional adoption acceleration: Banks and enterprises have been waiting for regulatory clarity before diving deeper into DeFi integrations

- Reduced compliance costs: Standardized requirements mean less legal uncertainty and fewer surprise regulatory bills

The biggest win? You can finally build long-term product roadmaps without constantly looking over your shoulder for regulatory curveballs.

Impact of GENIUS Bill on Fintech Startups

Fintech startups operating in the international payments space have been caught between two worlds – traditional banking regulations and emerging digital asset rules. The GENIUS Bill could bridge that gap.

Key benefits for fintech innovators:

- Streamlined international compliance: One set of rules for stablecoin-based cross-border payments instead of navigating 50 different state requirements

- Faster product launches: Clear regulatory frameworks mean shorter legal review cycles and quicker time-to-market

- Enhanced partnership opportunities: Traditional financial institutions will be more willing to integrate with compliant fintech solutions

For startups tackling multi-currency transactions and cross-border payment challenges, this regulatory clarity could be the difference between scaling successfully and getting stuck in compliance limbo.

What B2B Payment Platforms Need to Know

B2B payment platforms have been particularly hamstrung by regulatory uncertainty. Your clients need reliable, scalable payment infrastructure, but unclear rules around digital assets have made it risky to innovate with stablecoins and blockchain technology.

The GENIUS Bill addresses your biggest pain points:

- Cross-border payment clarity: Defined rules for using stablecoins in international B2B transactions

- API integration standards: Clearer guidelines for building compliant payment APIs that work with digital assets

- Client confidence: Your enterprise clients will be more comfortable adopting innovative payment solutions with clear regulatory backing

This is especially important for platforms handling marketplace payouts, vendor disbursements, and other complex third-party payment workflows where regulatory uncertainty has been a major barrier to adoption.

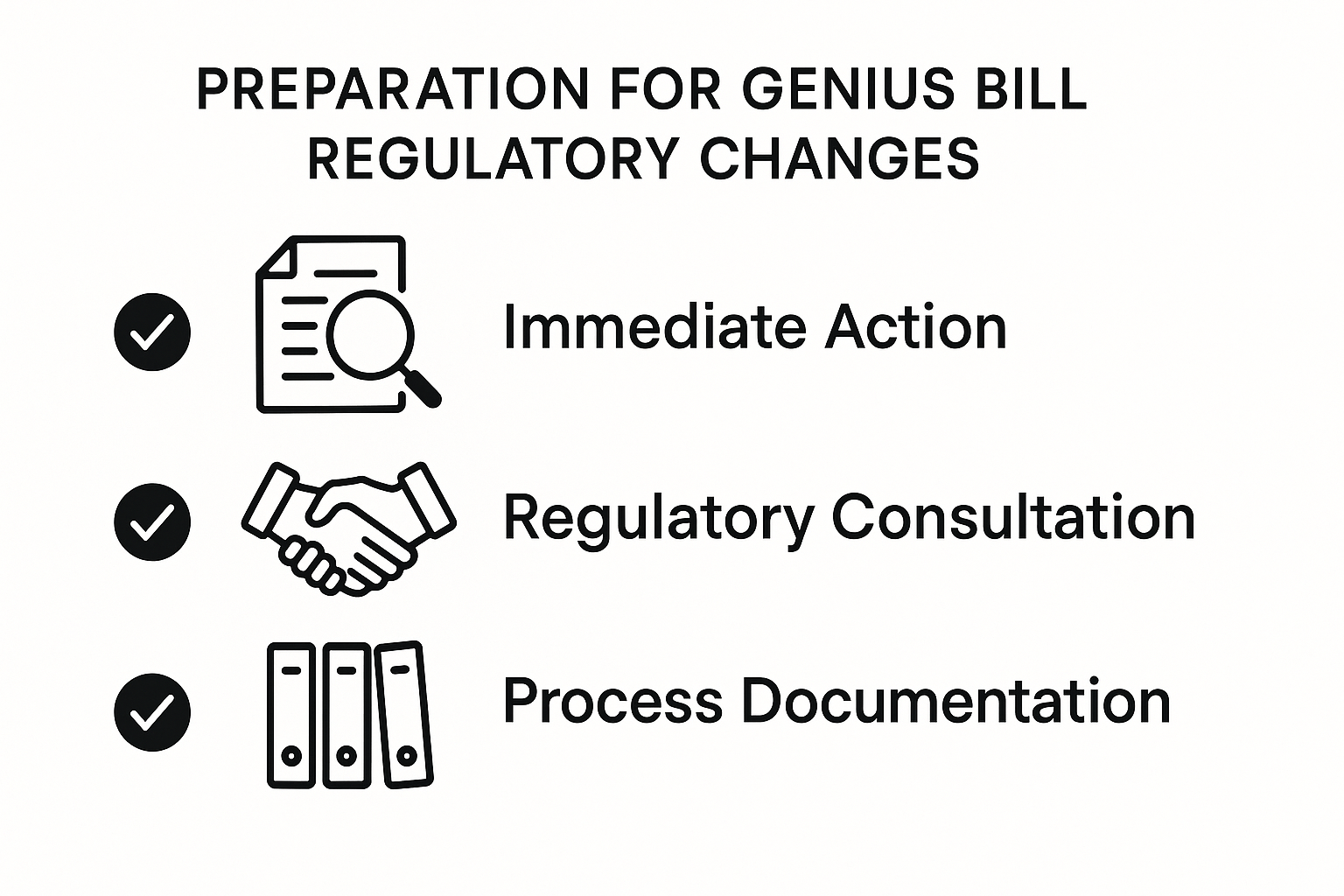

Preparing for the New Landscape

Whether the GENIUS Bill passes or not, the crypto and payments legislation landscape is evolving rapidly. Here's how to prepare:

Immediate steps:

- Audit your current compliance framework – identify gaps that clearer stablecoin regulation might address

- Engage with regulatory experts – now is the time to build relationships with legal teams who understand digital asset compliance

- Document your processes – clear regulatory frameworks reward companies with well-documented compliance procedures

Strategic considerations:

- Infrastructure flexibility: Ensure your payment systems can adapt to new regulatory requirements without major overhauls

- Partnership evaluation: Consider how regulatory clarity might open new integration opportunities with traditional financial institutions

- Product roadmap alignment: Plan product development around anticipated regulatory frameworks rather than trying to work around uncertainty

The Bottom Line: Clarity Creates Opportunity

The GENIUS Bill vote represents more than just another piece of legislation – it's a potential catalyst for innovation in the fintech and Web3 space. Regulatory clarity doesn't stifle innovation; it enables it by creating a predictable environment where companies can build confidently.

For fintech startups, this could mean faster scaling and easier access to traditional financial partnerships. For B2B payment platforms, it opens the door to more sophisticated cross-border solutions. For Web3 companies, it provides the legitimacy needed for mainstream adoption.

The key is being ready to move quickly when that clarity arrives. Companies that have prepared their compliance infrastructure and built flexible, scalable platforms will be first to market with next-generation solutions.

Call-to-action: Ready to future-proof your payment infrastructure for the evolving regulatory landscape? Book a demo with Cybrid to see how our compliant-by-design platform can help you scale confidently, regardless of what regulatory changes lie ahead.